India - Personal loan - online with instant disbursal.

- Get link

- X

- Other Apps

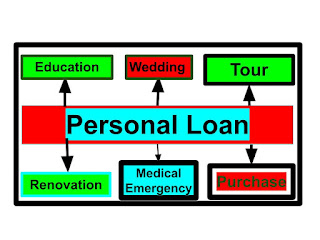

Introduction: Most people want to do something that makes them happy, healthy, and wealthy. Such types of many occasions come in our life as given below: For our happiness, we want to enjoy our holidays, and vacations with our family members, relatives, and friends. For this, we want to make a luxurious and memorable plan for our tour and travel. To meet the expenses for our dream, we do not wish to dispose of our assets, instead, we want to pay a monthly installment of expenditures for a year or more. Wedding functions, home renovations, higher education, online courses, etc. are the other occasions when we want to spend a lot of money to make memorable, joyful, and wise choices. Again here we want to pay in monthly installments instead of paying a lump sum amount by eroding our assets. One different type of occasion may come to us like a medical emergency when we need a good amount of money all of sudden to meet the demand. In the above-mentioned scenarios, a Personal Loan is the one the viable solution to meet the demand. In this blog, we will discuss the best options for personal loans available in India. Come on, start the journey of personal loans, now. |

What is a personal loan? A personal loan is a multipurpose loan that allows funds for varied financial uses like weddings, home renovations, travel, tours, holidays, vacations, hotel stays, medical emergencies, education, online courses, purchase of consumable or luxury items, Repay or consolidating the loan, etc. It has an easy application process, and quick disbursal, to avail of the funds efficiently and immediately for any need. The lender bank verifies the borrower’s creditworthiness to provide them with such loans. So, if you have a good credit score, then a personal loan can be your friend in need. |

The following features of the personal loan are important: Interest rate. Loan amount limit. Loan tenure limit. Processing fee. Foreclosure charges. Miscellaneous charges. Terms and conditions. |

What are the eligibility criteria for a personal loan? Eligibility criteria for getting a personal loan vary from lender to lender, however, in basic terms, some criteria are described below: A comprehensive assessment of an individual's financial profile, age, credit score, income, employment history, and existing debt or obligations determine Personal Loan eligibility. A good credit score, stable income, and a low debt-to-income ratio increase your loan amount and quick approval and disbursal. How much personal loan amount do you get from the lender? It depends on the above-mentioned factors. Personal Loan Eligibility is the assessment of an individual's qualifications for obtaining a Personal Loan. Check your eligibility (maximum permissible personal loan amount) using the online personal loan eligibility calculator of different banks, NBFCs, or authorized lenders.

Prospective borrowers are encouraged to utilize these tools to get the Personal Loan eligibility check before formally applying for a Personal Loan.

Review and check Personal Loan eligibility results carefully. Consider factors like interest rates, tenure, and other terms associated with the loan before deciding to borrow. Understanding and optimizing these factors will make a successful Personal Loan eligibility check and a smoother application process. If you find the calculated loan eligibility suitable, you can proceed with the loan application process through the bank's website, or app or visit a nearby branch for further assistance. We will elaborate on these terms further in the next section for better understanding: |

Age: Age determines Personal Loan eligibility. It may be between 21 to 60 years of age or may vary lenders-to-lenders. |

Credit Score and history of repayment: A higher credit score and consistent repayment history of the loan show responsible financial behavior improves eligibility and often reduces the interest rate. |

Employment Status: The eligible amount for a personal loan and interest rate also depends on your Employment, experience & stability with an MNC, public/private limited company, government, or Public sectors. A good profile increases the chances of a high amount for a personal loan and a low rate of interest. |

Monthly Income: It is one of the main criteria to decide the personal loan amount and its interest rate. Stable and high monthly income will impact the loan amount, and interest rate also. |

Debt-to-income ratio: Existing financial commitments and a balanced debt-to-income ratio will affect eligibility. Higher balanced loans may put you in a high interest rate category due to the high risk of repayment. |

Relationship with the lender: Long-term and good relationships with the lender may give you a suitable loan amount and interest rate on favorable terms. You may be considered the pre-approved loan. |

Market Trends and RBI Policies: Various economic factors, market conditions, and RBI policies influence the overall interest rate, terms, and conditions. Changes in repo rates and other economic indicators can affect the interest rates also. |

What factors can affect your loan EMI? The following factors can affect your loan EMI: Loan Amount: The higher the loan amount, the higher the EMI payable. Rate of Interest: In this case, too, the rate of interest is directly proportional to the EMI. The higher the rate of interest, the higher the EMI.

Loan Tenure: The loan tenure you choose is inversely proportional to the EMI. The longer the tenure, the lower the EMI. However, with longer tenure, you may end up paying more as interest. Online calculators are provided by the lenders and third-party websites and apps. By filling in the data on the calculator, You can easily understand the suitability by adjusting the EMI, tenure, and loan amount as per your need and repayment capacity. |

Is it possible to apply for a joint Personal Loan? Yes, you can apply for a Personal Loan jointly with your spouse, or any other family members like parents or siblings. One of the benefits of applying for a Personal Loan with a co-borrower is that the lenders will consider both the applicants’ income while determining the loan amount. This means that you can apply for a higher loan. However, you must know that if the co-borrower has a poor credit history, there is a risk that the lender might reject your loan application. |

How can you get a personal loan instantly, without a physical visit to the bank? Various banks have different procedures to get the personal loan, however, a general procedure to get quick disbursal of personal loans without visiting the lending bank is given below: To get a Personal Loan immediately, apply online. Securing a Personal Loan online swiftly is a hassle-free process. Here are the steps: Visit the website or mobile app of the lenders. Go to the Personal Loan section and click Apply Now. Fill in the Application: Complete the online application form by entering your personal and financial details. Document Submission: Upload the necessary documents digitally. This convenience speeds up the verification process. Instant Approval and Disbursal: An efficient evaluation process allows instant approval. After approval, the loan amount is disbursed to your account, often within a few hours. Before applying, use the Personal Loan EMI Calculator to calculate your EMIs based on the loan amount, tenure, and interest rate. Also, read the terms and conditions carefully. |

Whether insurance cover is needed for a personal loan? While opting for a Personal Loan, insurance cover for a personal loan is not generally mandatory but it is highly recommended to add the insurance coverage for your loan for the wellbeing of the family in case of mishappening as described here:

When you apply for a personal loan, considering insurance can be a prudent step in safeguarding your financial well-being. Insurance for a personal loan provides coverage in events like accidental death, permanent disability, or loss of employment. In the unfortunate event of such occurrences, the insurance ensures that the loan is repaid without placing undue financial strain on the borrower's family. EMI and Insurance: When you utilize the Personal Loan, the cost of insurance is not typically included in your EMI. If you opt for loan insurance, the premium may be charged as a separate, one-time fee or added to the total loan amount, depending on the policy terms. |

What is a Personal Loan Overdraft Facility: A personal Loan Overdraft allows the customers to withdraw funds as per requirement, and pay interest only on the used amount for the utilization period. This option is handy for meeting pressing needs or managing unexpected expenses. A Personal Loan Overdraft guarantees you have immediate access to funds without the higher costs typically associated with other loans. Interest rate, overdraft amount, and terms and conditions vary from lender to lender. |

What is a credit score or CIBIL score? A credit score of CIBIL {Credit Information Bureau (India) Limited} Score is a 3-digit numeric summary of your credit history, rating, and report, and ranges from 300 to 900. The closer your score is to 900, the better your credit rating is. |

Does personal loan inquiry affect the credit score? When an applicant applies for a loan, the authorized lender will fetch his credit report from the credit bureaus. Such lender-initiated credit report requests used for evaluating loan applications are considered hard inquiries. The credit bureaus in turn would slightly reduce the credit score for each hard enquiry. Hence, if an applicant applies for a personal loan with multiple NBFCs, banks, or authorized lenders within a short span, his credit score may register a deeper reduction. Instead, personal loan applicants should visit online lending marketplaces to compare personal loans offered by multiple lenders and apply accordingly. While lending marketplaces would also fetch the credit report of the loan applicant, such inquiries are known as soft inquiries and do not affect the credit score of the applicant. |

Does a personal loan affect the credit score? Yes, personal loans availed from authorized lenders will have an impact on the credit score of the applicants. A personal loan can impact your CIBIL score either negatively or positively. If taken while already in debt, it can have a negative impact. At the same time, its timely repayment will boost your overall score. |

How to Improve Your Chances of Getting a Personal Loan? Credit Clean-up: One of the main factors taken into consideration by lenders is your credit score. Getting a personal loan is easier with a high credit score. If your score is low, you must check your reports to see if there are any errors. Sometimes, simple errors could hurt your scores, and if you find any of these, you must report them to CIBIL. Rebalancing your income and debts: Lenders ask for proof of income when you apply for personal loans to ascertain your debt-to-income ratio. Consider the sale of liquid assets like stocks or earning more through a part-time job to increase your annual income. Doing so will increase your debt-to-income ratio and increase your chances of getting a loan. Consider Co-signers or Guarantors: If you are finding it hard to get a personal loan on your own accord, you can apply for one by adding a co-signer (joint borrower) or guarantor. The person you choose as a guarantor must have a good credit score (CIBIL score should be 750 or above).

Choose the Right Lender: Every lender has their own requirements when it comes to credit scores and income. When looking for personal loans, pick a lender whose eligibility criteria you meet and apply accordingly. The problem with applying with multiple lenders is that each of them will check your credit score, and each time your full credit report is pulled out, your credit score drops. Therefore before applying, select the best personal loan and apply for that only. |

Should I Prepay My Loan Early? When a borrower pays their loan off in entirety or partially before the payment is due, it is known as prepayment of loan. Even though prepayment may provide peace of mind to the borrower, it might not be financially beneficial due to various terms and conditions imposed by the lender. Therefore it is necessary to compile all the pros and cons of prepayment. After calculation, if it is found that the prepayment is beneficial, then you may go ahead with that. |

List of the lenders: Several lenders: Public Sector Banks, Private Banks, Regional Rural Banks, Small Finance Banks, Cooperative Banks, Payments Banks, Non Banking Finance Companies (NBFCs), and other authorized lenders or apps are registered with RBI for offering personal loans with defined terms and conditions. Some of the lenders are listed below: | |

PSU (Government) Banks | |

State Bank of India (SBI) | Bank Of Baroda (BoB) |

Punjab National Bank (PNB) | Indian Overseas Bank (IOB) |

Union Bank of India | Canara Bank |

Indian Bank | Uco Bank |

Central Bank of India (CBI) | Bank of India (BoI) |

Bank of Maharashtra | Punjab & Sind Bank |

Private banks | |

Axis Bank | Bandhan Bank |

CSB Bank | City Union Bank |

DCB Bank | Dhanlaxmi Bank |

Federal Bank | HDFC Bank |

ICICI Bank | IndusInd Bank |

IDFC First Bank | Jammu and Kashmir Bank |

Karnataka Bank | Karur Vysya Bank |

Kotak Mahindra Bank | IDBI Bank |

Nainital Bank | RBL Bank |

South Indian Bank | Tamilnad Mercantile Bank |

YES Bank | |

Some of the NBFCs and other lenders: | |

Tata Capital Limited | Piramal |

Home Credit | DHANI |

SMFG India | Muthoot Finance |

L&T Finance | HDBFS Personal Loan |

CASHe | MoneyTap |

Kredtibee | Moneyview |

Early Salary | Aditya Birla |

Shriram Finance | Navi |

DMI Finance | BFIL |

KSFE | TurboLoan powered by Chola |

MyShubhLife | Fullerton |

FlexiSalary Instant Loan App | InCred Personal Loan |

Edelweiss Salaried Personal Loan | MobiKwik ZIP |

Lendbox Hero FINCORP | NORTHERN ARC |

Vivriti capital | Mahindra Finance Personal Loan |

mPokket | NIRA Finance |

ZestMoney | Buddy loan |

Lazypay | Freopayneu |

AmazonPay | MyLoanCare |

Kreditzy | Tata Neu App |

Credy | Finnable |

FairMoney | Privo |

DigiMoney | CapitalFloat |

Poonawala finance | PhonePe |

Lendingkart | Flipkart Finance |

Stashfin | Rupee Redee |

Branch Loan App | Rufilo Loan App |

Fibe | Smart Coin Loan App |

Slice | IBL Finance |

For a better understanding of personal loans, the terms and conditions of some of the lenders are listed below: | |

Terms and conditions of some of the lenders (NBFCs & Apps based): | |

Various NBFCs provide personal loans with variable interest rates, tenure, terms & conditions. Interest rates may start from 10.49% per annum. The maximum Loan amount may be around Rs. 35 lahks and the maximum tenure may be 5 years. Many NBFCs also offer pre-approved instant personal loans to selected customers. | |

Eligibility criteria for personal loans offered by NBFCs: Eligibility criteria for personal loans vary from company to company. However, the general criteria are given below: | |

The applicant should be 21 years old at the time of loan application and 70 years old at the time of loan maturity. Indian residents are eligible for personal loans from NBFCs. Salaried individuals working with public and private sector companies, employees of State/Central/Local government, self-employed professionals, and self-employed non-professionals are eligible for personal loans. Minimum monthly income: usually Rs 15,000 (some lenders might ask for higher monthly income.) Credit Score: It should be at least 750. 750 and above can increase the chances of availing personal loan at lower interest rates. However, some NBFCs offer personal loans to applicants with credit scores below 750, at usually higher interest rates. | |

Documents Required for Personal Loan Application: The requirement varies from company to company. However, in general terms, some of the following documents are required to avail of the personal loan. Duly filled application form with photographs. Identity Proof- Anyone: PAN Card, Voter ID card, Driving License, Aadhaar Card or Passport. Age Proof- Anyone: Aadhar Card, Birth Certificate, SSC Certificate, Voter ID card or PAN Card. Address Proof- anyone: Aadhar Card, copy of ration card, Voter ID card, Driving License, Passport, electricity bills, or gas connection bills. Bank account statement for the past 6 months. Salary slips for the last 3 months. Form 16/ITR for the last 3 years. | |

Tata Capital Limited | |

Maximum Loan Amount ₹35 lakh | Rate of Interest Starts from 10.99 % per annum |

Maximum tenure 6 Years | Processing Fee 0.0% - 5.5% |

Minimum Monthly Salary | Rs 20,000 (Rs 15,000 for Government Employees, Salaried Employees, Women, Travel Loan) |

Processing Fee | Up to 5.5% of the loan amount |

Tata Capital Limited offers special personal loan schemes like Personal loans for Women, Personal loans for Government Employees, Personal loans for Travel, Personal loans for Medical, Personal loans for Marriage, Personal loans for Self-employed and Salaried and Personal loans for Home Renovation, etc. | |

Tata Capital Limited also offers a Personal loan Overdraft facility at an interest rate of 14.75% p.a. | |

DMI Finance: | |

Maximum Loan Amount ₹25 lakh | Rate of Interest Starts from 12 % per annum |

Maximum tenure 5 Years | Processing Fee Maximum 4% |

PaySense: | |

Maximum Loan Amount ₹ 5 lakh | Rate of Interest Starts from 16 % per annum |

Maximum tenure 2 Years | Processing Fee Maximum 3% |

Muthoot Finance: | |

Maximum Loan Amount ₹ 10 lakh | Rate of Interest Starts from 14% per annum |

Maximum tenure 5 Years | Processing Fee Maximum 2% |

TurboLoan powered by Chola: Loan Amount: ₹1L -₹3 Lakh Fixed interest rate: 15.00% - 21.00% Tenure: Up to 3 Years Processing Fee: 3.00% | |

Fullerton Personal Loan: Loan Amount: Up to ₹25 Lakh Fixed interest rate: 11.99% Tenure: 5 Years Processing Fee: 6.00% | |

Aditya Birla Capital Personal Loan: Loan Amount: Up to ₹50 Lakh Fixed interest rate: 10.99% per annum. Tenure:7 Years Processing Fee: 3.00% | |

India Infoline Finance Ltd. Personal Loan: Loan Amount: Up to ₹5 Lakh Fixed interest rate: 12.75% - 44.00% per annum. Tenure: 4 Years Processing Fee: 2.00% - 6.00% | |

Bajaj Finserv Personal Loan: Loan Amount:: Up to INR 40 Lakhs Tenure: 12 to 60 months Rate of Interest: starts from 11% per annum. Processing Fee: Up to 3.93 % of the loan amount ( inclusive of GST). | |

Personal loans offered by lending banks in India: Almost all the lending banks (Public sector, Private, small finance, and Cooperative banks) in India offer personal loans on varying terms and conditions. Some of the banks offering personal loans are listed below: | |

Personal loans offered by Kotak Mahindra Bank: | |

Special features: Person loans up to 40 lakhs with instant disbursal. Minimum Documentation. Eligible customers can get the pre-approved personal loan within no time (No paperwork, instant approval, and immediate disbursal). Customized Tenure 1 year to 6 years. You can apply online for instant personal loans. The quick and hassle-free application process to get the funds within no time. No guarantor is required. Zero collateral ( no need to mortgage the property). An overdraft facility on personal loans is available. The interest rate starts from 10.99%. Digital KYC ( online easy documentation with video KYC using an Aadhaar card). Personal loan funds can be used for various purposes like marriage loans, travel loans, medical emergency loans, home renovation loans, debt consolidation, kickstarting the business, purchasing luxury items, etc. Insurance coverage for personal loans is not mandatory. However, it is advised to take it for the wellbeing of the family in case of any mishappening. Kotak Bank has various options to add insurance coverage. | |

Documents required: A valid Identity (ID) proof like a passport, PAN card, Driving license, or Voter ID card. A valid residence proof like a passport, driving license, or Aadhaar card. Three months' bank statements showing your income details. 2-3 passport-size photographs. For salaried customers, 3 months salary slips. Kotak Mahindra Bank offers the convenience of pre-approved Personal Loans for our existing customers, even without the need for a salary slip. These pre-approved loans are designed to provide quick financial assistance based on your relationship with the bank and your financial history with us. It simplifies the personal loan application process, making it faster and hassle-free, as the bank already possesses your financial details and repayment capacity. | |

Example of EMI calculation: | |

Loan amount (in Indian Rupees) | INR 100,000 |

Interest rate (% per year) | 10.99% |

Tenures ( in years) | 01 year |

EMI (Equated monthly installment) | INR 8837 per month |

Processing fee: Nonrefundable, up to 3% of the final loan amount plus taxes, will be deducted from the loan amount at the time of disbursal. | |

Penalty on overdue EMI: Unpaid amounts on respective due dates shall attract penal charges @ 8% per annum (to be charged for actual no. of days) on overdue amount plus applicable taxes. | |

Swap charges, i.e. charges for change in repayment mode, repayment instrument, or EMI date: INR 500/- plus taxes per instance. | |

EMI dishonor/Bounce charges: INR 750/- plus taxes per instance. | |

Lock-in period: No lock-in period for Kotak Personal loans post payment of the first EMI. | |

Foreclosure Charge: Up to 3 years: 4% + taxes, on outstanding principal. After 3 years: 2% + taxes, on outstanding principal. | |

Part pre-payment charges: Post-completion of 12 months : Part-Prepayment is allowed up to 20% of the Principal loan outstanding. It is allowed once a year. The charge per instance of part payment is INR 500 plus taxes. | |

Physical SOA (Statement Of Account) or Amortization (the gradual reduction of the debt through the repayments we agree with the lender,) statement:

Once in a year- No charge. Post that - INR 200 plus taxes per request. | |

Personal loan eligibility criteria: Nature of Employment: Salaried people working in MNC, public limited company, or private limited company. Age: 21 years to 60 years. Minimum Monthly Income: Kotak Bank Salary Account holders: ₹ 25,000 minimum net monthly income. Non-Kotak Bank Salary Account holders: ₹ 30,000 minimum net monthly income. Kotak Bank employees: ₹ 20,000 minimum net monthly income. Minimum Educational Qualification: Graduation / Diploma Work Experience: At least one year of work experience is required. | |

Personal loan offered by ICICI Bank: | |

Special features: Personal Loan limit: ₹50 Lakhs No foreclosure charges after payments of 12 EMIs. Minimal documentation. No Collateral is required. Fixed Interest Rates. The interest rate starts from 10.80% per annum. Flexible tenure (12 months to 72 months). | |

Multi-purpose Personal loan Example: Medical emergency. Marriage expenses. Home renovation. Appliances & Gadgets. Travel & tour. Education. Online courses. | |

Personal Loan eligibility criteria: For salaried applicants, the Personal Loan eligibility depends on their age, net salary, years of professional experience, and duration of residence at the current address. Self-employed individuals are assessed based on their age, minimum turnover, minimum profit after tax, business stability, and existing relationship(s) with ICICI Bank. These criteria collectively determine the eligibility for a Personal Loan, ensuring a thorough financial stability and credibility evaluation. Lastly, the applicant’s credit score may also be considered. Eligibility criteria can change as per RBI guidelines. In the coming sections, we are going to elaborate more. | |

Personal Loan eligibility criteria for Salaried individuals: Must be a resident of India. Good credit score. Age: Between 20 and 58 years. Salary Account with any of the banks in India. Net salary**: Minimum monthly income of Rs 30,000. (Individual regular monthly income) Total years of work experience: 2 years. Note: **The minimum salary requirement will differ depending on the profile (type of employer, having a relationship with ICICI Bank, etc.) of the customer. | |

Documents Required from a salaried employee: Salary slips for the last 3 months. Latest 3 months Bank Statement (where salary/income is credited). Proof of Identity/Residence: Any one of the below Official Valid Documents (OVD) can be accepted as Current / Communication address proof only. Passport Driving License issued by Regional Transport Authority Voter's Identity Card issued by the Election Commission of India Letter from National Population Register containing details of name and address Proof of possession of complete AADHAR Card NREGA Card. | |

Loan eligibility criteria for self-employed individuals: Proof of Identity/Residence: Any one of the below Official Valid Documents (OVD) can be accepted as Current / Communication address proof only. Passport Driving License Voter's Identity Card Letter from National Population Register containing details of name and address. AADHAR Card NREGA Card Age: Minimum age is 23 years, maximum age at the end of the tenure is 65 years. Maximum loan amount: Up to Rs 50 lakh. Income Proof : Audited financials for the last two years Latest 6 months bank statement. Proof of continuity of business. Business Vintage: 2 years in the current business and total experience >= 3 years. Office address proof. Proof of residence or office ownership. Note: ICICI Bank provides Loans to self-employed individuals under business installment loans. Conditions apply as per policy. ICICI Bank reserves the right to call upon additional documents at its discretion. | |

Personal loan EMI calculation ( ICICI Bank): | |

Loan amount (in Indian Rupees) | INR 100,000 |

Interest rate (% per year) | 10.80% |

Tenures ( in years) | 01 year |

EMI (Equated monthly installment) | INR 8829 per month |

Interest payable | INR 5946 |

Processing fee | Up to 2.00% of the loan amount plus applicable taxes. |

Personal Loan Eligibility: (Maximum permissible personal loan amount) | |

The ICICI Bank online Personal Loan Eligibility Calculator helps you to determine the maximum loan amount you can avail from the bank. An example is given below: | |

Monthly income | INR 75,000 |

Total existing obligation/EMI | INR 20,000 |

Loan tenure | 60 months |

Eligible total amount for personal loan | INR 10 to 11 Lakh (indicative) |

Quick steps for instant approval and disbursal of personal loan:

| |

Personal loan offers from HDFC Bank: | |

Special features: Quick funds = Express personal loan. Personal loan = get the instant loan online. Instant disbursal. Minimum paperwork. Transfer loan at lower EMI. Completely Digital process. Special rate for government employees. Pre-approved loan for selected customers. Personal loan maximum limit = 40 lakh. In special conditions, up to 75 lakhs. Tenure = 3 months to 72 months. Fixed Interest rate starts from 10.75%. Types of personal loans: Marriage, home renovation, salaried people, golden edge personal loan, medical emergency, especially for women and government employees, travel, teachers, etc. Processing fee = up to 4999 + GST Special offer for existing HDFC bank account holders. 24x7 assistance anywhere. CIBIL Score = 720 or more is better. No collateral or guarantor is required. Foreclosure of personal loans is allowed under some terms and conditions. Special offers of interest rates are also available regularly. Documents required: No documents are required for a pre-approved loan. Non-pre-approved loan = 02 latest salary slips, last 3 months' bank statement, and KYC. | |

Personal loan EMI calculation (HDFC Bank): | |

Loan amount (in Indian Rupees) | INR 100,000 |

Interest rate (% per year) | 10.75% |

Tenures ( in years) | 01 year |

EMI (Equated monthly installment) | INR 8827 per month |

Personal loan offered by Axis Bank: | |

Special features: Personal loans up to INR 40,00,000 Interest rate starts from 11.25% Online, paperless process. Minimal documentation. Tenure: 12 months to 84 months. Customized repayment options. Quick approval within no time. No collateral is required. Transparent terms and conditions. No hidden charges. Processing fee: up to 2% of loan amount + GST | |

Personal Loan eligibility criteria for Salaried individuals: Employees of: Central or State government, Public Sector Undertakings (PSUs), Local bodies, etc. Employees of Private and Public limited companies. Minimum age - 21 years. Maximum age - 60 years at the time of maturity of personal loan. Minimum net monthly income- INR 15,000 for existing Axis Bank customers INR 25,000 for other bank customers. | |

Documents required from salaried employees: Last three months' bank statements. Three latest salary slips with Form 16. KYC document (Any one of the following): Passport. Driving License. Voter's Identity Card Aadhaar Card with date of birth. PAN card. | |

Personal loan EMI calculation (Axis Bank): | |

Loan amount (in Indian Rupees) | INR 100,000 |

Interest rate (% per year) | 11.25% |

Tenures ( in years) | 01 year |

EMI (Equated monthly installment) | INR 8850 per month |

Break up of total payment: Principal amount: INR 100,000 Interest amount: INR 6198 Total amount payable: INR 106, 198. | |

IDFC FIRST Bank Personal Loan: IDFC FIRST Bank's personal loan interest rate starts from 10.99%p.a. Tenure: 1 to 5 years. Processing Fee: 2.00% - 6.00% The bank offers special personal loan schemes like Personal loans for Marriage, Travel, Emergency, Medical Loans, IDFC FIRST Debt Consolidation Loans and IDFC FIRST Small Personal Loans. Existing personal loan borrowers from other banks/NBFCs can transfer their loans to IDFC FIRST Bank at a lower interest rate with the Personal Loan Balance Transfer facility. | |

IndusInd Bank Personal Loan: Loan Amount: Up to ₹50 Lakh Fixed interest rate: 10.49% Tenure: 5 Years Processing Fee: Up to 3.00% | |

Standard Chartered Bank: Loan Amount: ₹1L -₹6 Lakh Fixed interest rate: 10.60% - 18.00% per annum Tenure:5 Years Processing Fee: 2.25% | |

Yes Bank Personal Loan: Loan Amount: Up to ₹40 Lakh Fixed interest rate: 10.99% - 20.00% per annum. Tenure: 5 Years Processing Fee: 2.50% |

Final words: Whether we avail of a personal loan? How much personal loan should we avail? What should be the tenure of a personal loan? Which lender is the best for a personal loan? Is there any possibility of fraud or hidden charges while availing the personal loan? These questions always come to our mind when going to avail of the personal loan. Here we will try to provide you with the answers as per my knowledge and belief. It may not be possible to fulfill all your requirements or desires without availing of the loan. Collateral loans or secured loans (where you are required to mortgage some property or assets) are considered best due to low interest rates. However, sometimes it may not be possible to avail of such loans due to a lack of required documents, shortage of time, due to urgent need, your requirement not falling under the secured loan, or some other reasons. Then to avail the personal loan is a good option to meet demand and it happens in life when it is required to avail the personal loan. How much personal loan is required? It depends on your personal needs. Calculate your loan requirement with the inclusion of all your expected expenses. Add roughly 10% to meet any left-out demand. For example, if your calculated need is INR 9 lakh, then avail INR 10 lakhs. Don't avail more than that, because its burden including handsome interest will come to you. What should be the tenure of a personal loan? Tenure is inversely proportional to the EMI amount. If you pay a higher EMI amount, tenure will be less, but at the same time, you have to calculate your monthly capability to pay the higher EMI amount. For example, after deducting all your monthly expenses, you are capable of paying INR 25,000 as EMI. You should minus 10 to 20% from this capacity to meet the unexpected need for a safe side. Therefore, your target for EMI should be fixed between INR 20,000 to 22,000. Accordingly, tenure should be opted.

Which lender is the best for a personal loan? Lenders providing low interest rates, customized tenure, customer customer-friendly terms and conditions may be our first choice. If we have so many suitable options then it may be an individual choice, but as an author, I am going to write my views as given below: I prefer the PSU (Government) banks due to their normally low interest rates and low miscellaneous charges, high trust in the government & transparency in terms and conditions. I may prefer the PSU bank which I already have a bank account, because it will do a fast disbursal of personal loans and it may give some privileges also. One thing is very negative with the PSU banks which I felt mostly and many times. That is a complicated and slow process. Moreover, comparatively fewer customer-friendly online processes, more visits to bank branches, less eligibility for personal loans, etc. Sometimes it is not possible to complete the complicated process or it may be humiliating or irritating. Therefore, Private banks may be my next preference. Several private banks in India, as listed earlier in this blog, are providing personal loans. I would prefer the one in which I already have a bank account. Bank having my salary account or business or current account will be the first choice, because private banks, especially having salary or business or current accounts, will provide the following facilities: low interest rate, maximum loan amount, instant approval and quick disbursal Minimum or no documentation Customer-friendly terms and conditions. Completely online and digitized process. No or minimum visit to the bank branch. Now, if both above options are exhausted, then the third preference may be NBFCs, which go through the interest rate, other charges, and different terms and conditions. Select the most suitable one. The next choice may be the small finance banks or cooperative banks. Go with the salary account bank if you are having the same. The last choice is the lenders (other than above mentioned options) authorized by RBI (Reserve Bank of India). Check thoroughly their authenticity, and select the best one. Is there any possibility of fraud or hidden charges while availing a personal loan? Yes, it may be. First of all check their authorization through Government websites, official websites, and other reliable sources. Their terms and conditions may or may not be customer-friendly. Select the best one very carefully. With the help of a third-party website or app - compare the personal loan interest, miscellaneous charges, and different terms and conditions. Select 3-4 options. After that cross-check from the government website, official website, and reliable sources. Now is the time to choose the best one. I think, after reading this blog, self-cross-checking will enable you to select the best personal loan. Good luck. | |

Disclaimer: This blog is written for educational and informational purposes only. The best efforts are made to provide real facts through self-knowledge, and after studying the following & similar websites. However, I do not take any responsibility and guarantee (legal or otherwise) for its correctness, completeness, consequences, or any typographical error. Data mentioned in the blog are subject to change from time to time. Before using the given information, cross-check the facts from reliable sources. Readers are requested to verify the authenticity, terms, and conditions of lenders from reliable sources before dealing with them. Avail the best one if needed as per your decision or take the help of an expert. https://www.newindianexpress.com ==The end==

|

- Get link

- X

- Other Apps

Comments

Post a Comment

Thank you, most welcome, 👍